Last updated 9 months ago

MarginDEX - AMM for Interest Rate Derivatives

Problem

Market Making of Interest Rate Derivatives is a very lucrative business for financial institutions. We will extend the AMM model on Cardano and showcase how trading can be automated in these products

Solution

Adapt the AMM technology to Interest Rate Derivatives and launch a DEX on the testnet to showcase its functionality. Executed FRA trades on the DEX and offload the managing of margin to BlockMargin

Total to date

This is the total amount allocated to MarginDEX - AMM for Interest Rate Derivatives.

About this idea

[Proposal setup] Proposal title

Please provide your proposal title

MarginDEX - AMM for Interest Rate Derivatives

[Proposal Summary] Budget Information

Enter the amount of funding you are requesting in ADA

99975

[Proposal Summary] Time

Please specify how many months you expect your project to last

12

[Proposal Summary] Translation Information

Please indicate if your proposal has been auto-translated

No

Original Language

en

[Proposal Summary] Problem Statement

What is the problem you want to solve?

Market Making of Interest Rate Derivatives is a very lucrative business for financial institutions. We will extend the AMM model on Cardano and showcase how trading can be automated in these products

[Proposal Summary] Project Dependencies

Does your project have any dependencies on other organizations, technical or otherwise?

No

Describe any dependencies or write 'No dependencies'

No dependencies

[Proposal Summary] Project Open Source

Will your project's outputs be fully open source?

No

License and Additional Information

Not open source

[Theme Selection] Theme

Please choose the most relevant theme and tag related to the outcomes of your proposal.

DEX

[Campaign Category] Category Questions

Describe what makes your idea innovative compared to what has been previously funded (whether by you or others).

An AMM for interest rate derivatives on Cardano is groundbreaking because it merges the world’s largest financial market with on-chain DeFi infrastructure.

Unlike traditional OTC and clearinghouse models, it enables transparent, permissionless, and continuous trading without intermediaries.

For Cardano, it’s a first-of-its-kind high-value use case; for the broader blockchain space, it pioneers fully decentralized rate derivative markets, redefining efficiency and access in global finance.

Describe what your prototype or MVP will demonstrate, and where it can be accessed.

MarginDEX will extend the functionality of BlockMargin that is currently running on https://blockmargin.app/trade

We have showcased BlockMargin to traders and risk managers at financial institutions as well as leading interest rate brokers and received positive feedback on the innovative nature of this application

A new section will be added to the dashboard where users will be able to provide liquidity and trade against existing liquidity pools. It will extend the functionality of the Order Book.

Describe realistic measures of success, ideally with on-chain metrics.

The MarginDEX app that we will launch on the testnet will be the result of R&D on how best to implement an AMM for Interest Rate Derivatives. A model of how this word currently does not exist for these types of instruments and we will need to use a novel approach

A successful outcome would be:

- A user is able to create a Forward Rate Agreement (FRA) against a predefined maturity point

- This automatically matches the user with a counterparty that takes the other side of the trade (DEX functionality)

- The managing of Margin is managed through BlockMargin

[Your Project and Solution] Solution

Please describe your proposed solution and how it addresses the problem

Interest rate derivatives differ from single-asset derivatives like those based on stocks, bonds and crypto assets because their value depends on an entire interest rate curve - a set of rates across different maturities - rather than a single market price. This means its pricing and risk management involve shifts in the whole curve, not just movements in one asset’s value.

Most AMMs today are designed for single-price assets, using formulas like constant product or stableswap curves. These models assume one price point for liquidity provision and trading, which doesn’t translate well to interest rate derivatives. Here, liquidity needs to account for the curve’s shape, multiple maturities, and how trades affect different points along it.

As a result, an AMM for interest rate derivatives must be built with models that capture curve dynamics, allow pricing along multiple tenors, and handle the more complex payoff structures—something that requires a fundamentally different approach from existing single-asset AMMs.

Cluster of AMMs

One way to adapt AMMs for curve-based pricing in interest rate derivatives is to use a cluster of AMMs, where each pool is dedicated to a specific maturity (e.g., 1M, 3M, 6M, 1Y). This approach breaks the interest rate curve into discrete points, allowing each AMM to price and provide liquidity for its own tenor. Together, the cluster replicates the full curve while keeping pricing and risk local to each maturity, making the system simpler to model and more capital efficient than a single complex curve-wide AMM.

Curve-wide AMM

A curve-wide AMM that provides liquidity for interest rate risk rather than for specific maturities. In this model, trades are expressed in standardized “risk units” (e.g., DV01), which represent the sensitivity of a position to movements along the interest rate curve. Each transaction is converted into these units, which are then drawn from a shared liquidity pool. This allows a single pool to support the entire curve, letting liquidity providers back all maturities at once while the AMM dynamically prices and manages how each trade impacts the curve’s shape.

Both of these methods are innovations on top of a classic AMM and as a result we will need to go through some degree of trial and error to identify which works better

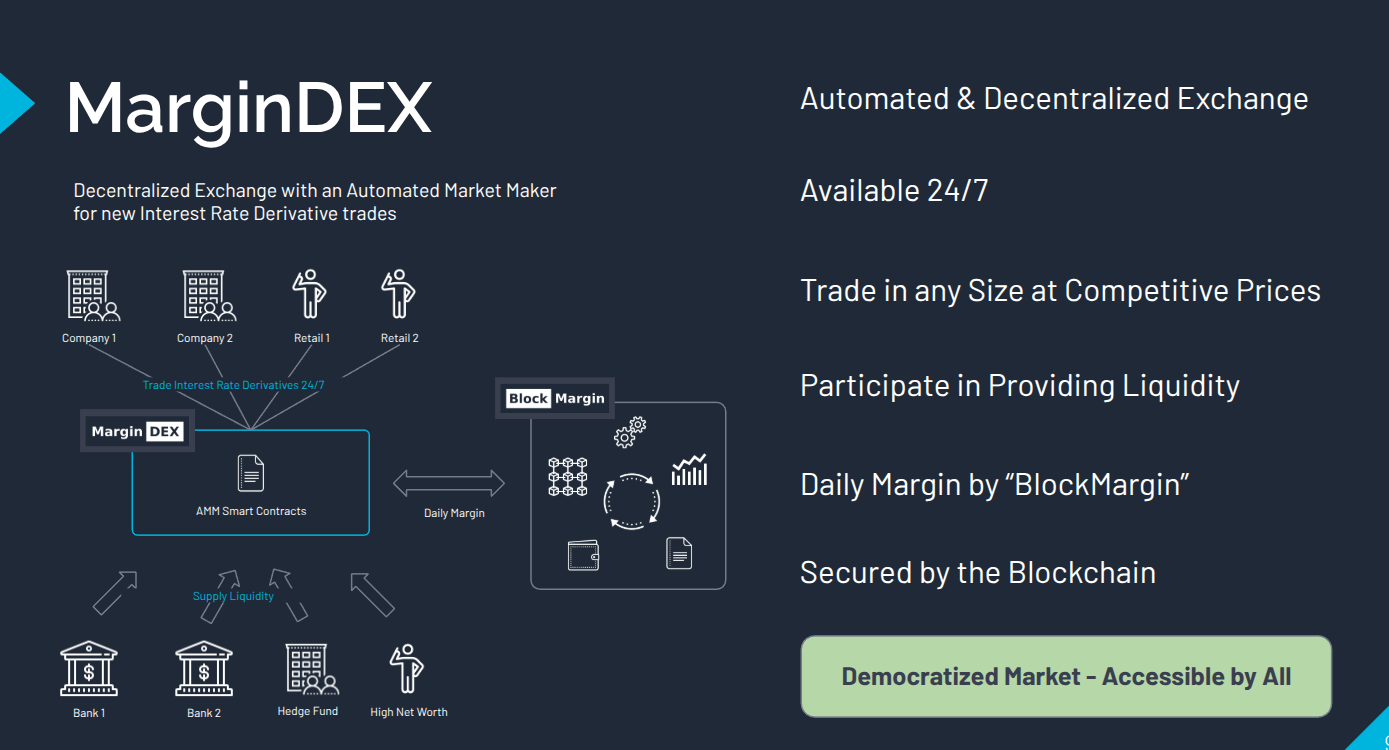

Integration with BlockMargin

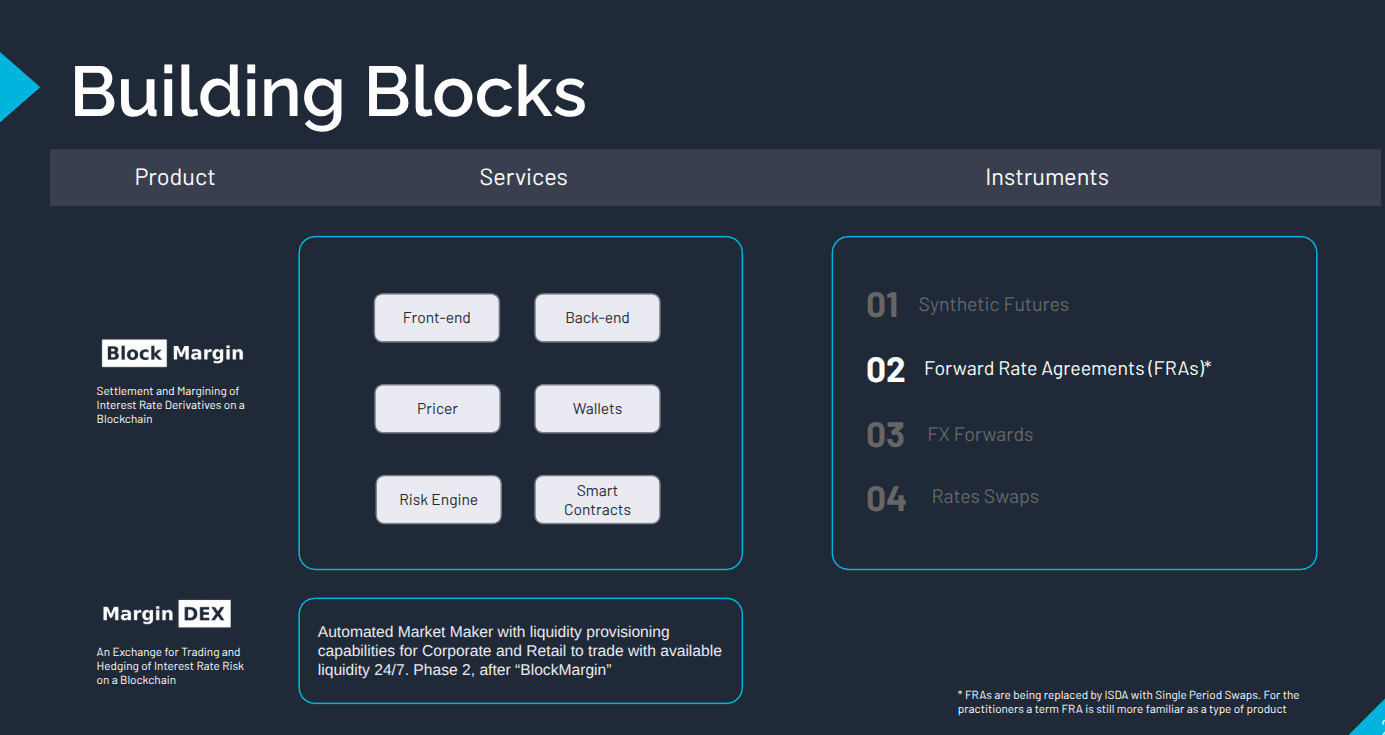

Over the last year we have been working on a platform called BlockMargin to manage the settlement process for interest rate derivatives. MarginDEX is the next evolution of this platform to build a DEX on top of BlockMargin.

Think of MarginDEX as the marketplace and BlockMargin as the delivery mechanism. MargiDEX is where trades are initiated, buyers and sellers are matched and then BlockMargin is the delivery vehicle that ensures the correct management of Margin throughout the life of the contract.

Significance of Margin Posting:

Understanding why margin matters is pivotal to appreciating the BlockMargin solution. Interest rate derivatives involve dynamic contract values that can turn positive or negative at any point. Margin posting becomes essential to prevent defaults and provide compensation if one party decides to exit the contract prematurely. Additionally, margin posting aids in avoiding litigation, as both parties can walk away, leaving margin with the counterparty to cover any adverse market moves.

[Your Project and Solution] Impact

Please define the positive impact your project will have on the wider Cardano community

MarginDEX is a first-of-its-kind platform - both on Cardano and across other blockchains. It builds on the innovation of Automated Market Makers (AMMs) and applies it to traditional financial instruments widely used in traditional finance (TradFi).

A successful launch will not only showcase Cardano’s capabilities but also attract significant attention from the TradFi sector.

Historically, AMMs have been designed for account-based blockchains like Ethereum, and required adaptation to work on UTXO-based blockchains such as Cardano. Through the BlockMargin project, we’ve successfully leveraged the UTXO model to manage margin for existing interest rate derivative trades. With MarginDEX, we’re taking the next step - designing an evolved AMM model specifically for trading interest rate derivatives within a UTXO framework.

The proposal will further validate the possibility of trading interest rate derivatives on Cardano (a completely new product on Cardano and other blockchains) and can potentially bring the financial services industry onto Cardano.

This proposal targets the traditional finance sector and aims to bring some of their operations onto the blockchain and create a Decentralized Finance alternative (DeFi)

It will increase the Total Value locked, total number and active daily users. And it will bring the largest market in the world onto a blockchain.

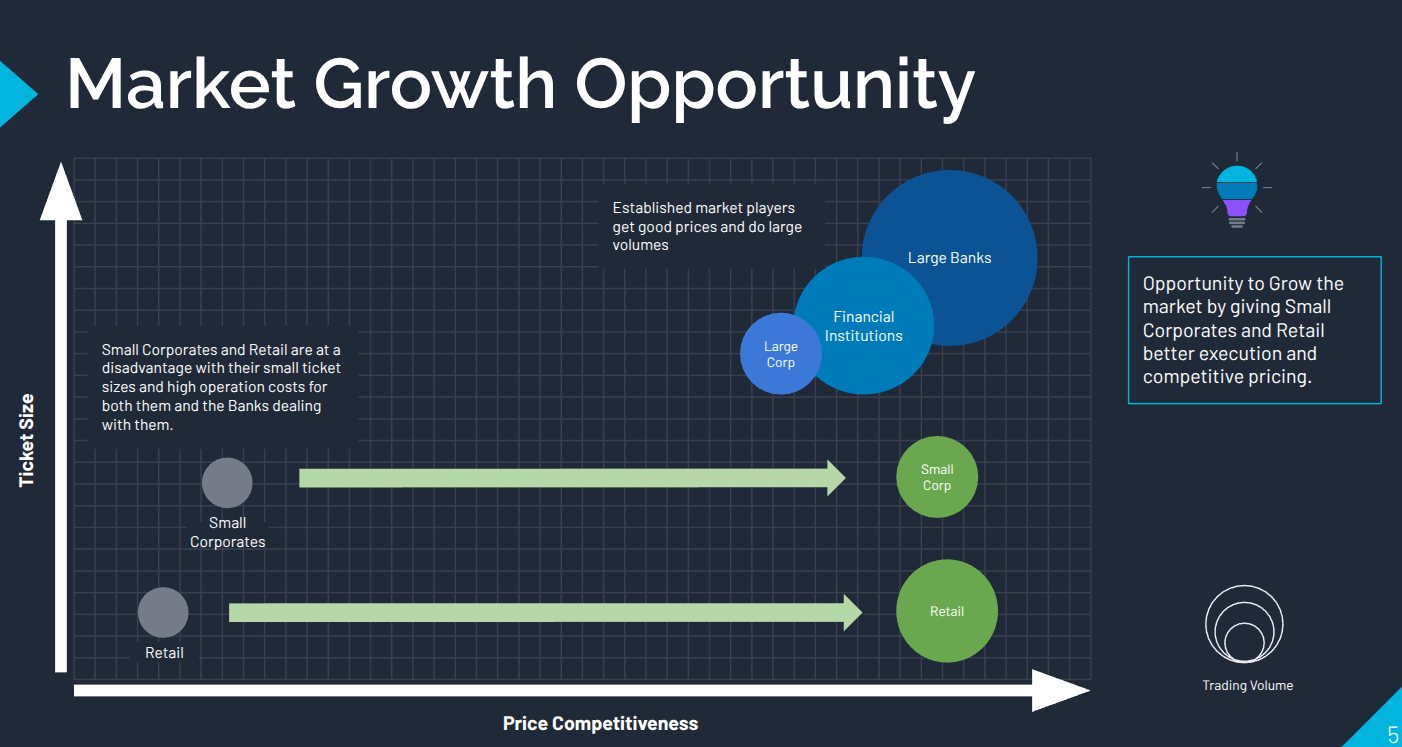

The Interest Rate Derivative market is the largest market in the world by a big margin, with $250+ Billion daily volume between Small Corporates, Retail and Financial institutions. The overall market that includes large corporations is even bigger at over $5 trillion of volume per day.

Bringing the market making, trading and settlement of these derivatives onto a blockchain has the potential to open up adoption of the large financial sector on a blockchain and, over time, drive a tide of adoption to that blockchain.

Settling these trades on the blockchain, reduces their operational cost drastically, making it possible for financial institutions to offer these products to smaller clients they overlooked in the past. This can lead to market growth as new participants enter the market.

There are significant growth opportunities for the mid-tier and corporates and retail customers who are currently priced out of this market that is dominated by large financial institutions.

Challenges Faced by Mid-tier Entities and Retail:

Interest Rate Derivatives serve as crucial risk management tools for corporations and asset managers, enabling them to hedge interest rate risks associated with loans, bond issuance, and other liabilities. However, small corporates and private individuals often find themselves excluded from this market due to the intricate back-office processes involved, particularly the daily margining requirements. Without the resources to handle daily margining, these entities face inflated fees imposed by financial institutions, leading to elevated credit and operational risks.

[Your Project and Solution] Capabilities & Feasibility

What is your capability to deliver your project with high levels of trust and accountability? How do you intend to validate if your approach is feasible?

We are on the final milestone of the remaining project which is the building of BlockMargin on the testnet. This proposal is to continue its development and use BlockMargin in this proposals Margin DEX

The key team members, Dmitry and Sergio, have decades of experience with trading and settling these types of Interest Rate derivative contracts and have worked together at a large financial institution in the Netherlands

Dmitry spent over a decade in Risk Management and Trading, managing multi-million dollar positions for the bank and the bank’s clients. Sergio is a banking professional with hands-on expertise in Regulation and bank-to-corporate interactions. They both have deep connections in the industry necessary to convince large financial institutions to do a pilot.

AMM DEXs

The team has extensive knowledge of the operational intricacies of AMM DEX and their risks. We are providers of liquidity on existing Cardano and on other chain AMM DEXs

We have written extensively and taught university classes on AMM DEXs. A diagram below for university students with an example of an AMM for BTCUSDC:

Public articles written

https://dynamicstrategies.io/docs/automated-market-makers/

University lecture:

https://www.linkedin.com/feed/update/urn:li:activity:7360747744832950272/

[Milestones] Project Milestones

Milestone Title

Adapt AMM model for Interest Rate Derivatives

Milestone Outputs

Perform R&D on how to operationalize the Cluster AMMs and Curve-wide AMM in the UTXO model. We know that classic AMMs require a “batcher” to operate, so we will need to study if the same batcher is still required for our AMMs and how it would work for both types of approached

Layout in a diagram of how the following elements should interact between each other for each AMM model

- Liquidity provider’s wallet

- Newly minted “receipt” tokens during liquidity provision

- Buy vs Sell side

- Automatic rate adjustment (the rate needs to adjust if there is too much demand in one direction)

Address the following questions:

- Managing margin post execution

- How to deal with trades that require liquidity from more than one liquidity provider

- How to deal with concurrent trades against the same liquidity in the UTXO model

Acceptance Criteria

A diagram of how different elements described in the Output above interact between each other in a diagram, “pseudo” script of how a transaction should be built to provide liquidity and of a transaction that consumes liquidity

Evidence of Completion

A diagram and a description of how both types of AMMs should work (the Cluster of AMMs and Curve-wide AMM). A video walkthrough the diagram and discussion of the pros and cons of each approach.

Delivery Month

3

Cost

24993

Progress

30 %

Milestone Title

Implement Cluster of AMMs

Milestone Outputs

First we will implement an AMM for 1 maturity point, e.g. the 1 year maturity point on an interest rate curve. This will made available on our https://blockmargin.app website

Then we will expand the same method to other maturity points, we will do up to 5 maturity point to evidence that the implementation is working

The user will be able to connect with their Cardano web-wallet (e.g. Eternl) running on testnet and initiate a buy or sell FRA trade for any of the 5 maturity points. The liquidity provider will automatically take the other side of the trade.

If we identify that a batcher is required for this set-up then we will build a batcher that will aggregate transactions and execute a UTXO where liquidity is provided.

Acceptance Criteria

A web dashboard with the functionality to add liquidity to each of the pre-defined 5 tenor points of the curve. The liquidity provider should be able to add and remove liquidity

In a separate section of the dashboard a trader should be able to initiate a FRA trade against any of the 5 maturity points and be automatically matched on the other side with the liquidity provider. Example: if a trader is initiating a buy FRA, then the sell FRA should be automatically confirmed by the liquidity provider(s)

Evidence of Completion

A video walkthrough of a dashboard on a Cardano testnet and a successful execution of:

- Adding liquidity

- Withdrawing liquidity

- Performing a trade against available liquidity

Delivery Month

6

Cost

24993

Progress

50 %

Milestone Title

Implement Curve-wide AMM

Milestone Outputs

The Curve-wide AMM is a more advanced version of the AMM as it needs to take into account the difference in risk across the different maturity points on the curve when providing liquidity.

For liquidity providers, we will implement the ability to add liquidity to the whole curve, irrespective of maturity

A trader should then be able to trade against any maturity on the curve, and liquidity will be consumed based on the risk amount, rather than the notional amount

Acceptance Criteria

A web dashboard with the functionality to add liquidity to the whole curve. The liquidity provider should be able to add and remove liquidity

In a separate section of the dashboard a trader should be able to initiate a FRA trade against any maturity and be automatically matched on the other side with the liquidity provider. Example: if a trader is initiating a buy FRA, then the sell FRA should be automatically confirmed by the liquidity provider(s)

Evidence of Completion

A video walkthrough of a dashboard on a Cardano testnet and a successful execution of:

- Adding liquidity

- Withdrawing liquidity

- Performing a trade against available liquidity

Delivery Month

9

Cost

24993

Progress

80 %

Milestone Title

Integration with BlockMargin and Testnet Launch

Milestone Outputs

An assessment of which AMM model works better (the Cluster of AMMs, or the Curve-wide AMM)

The AMM will then be connected to BlockMargin on the Cardano testnet to manage the margin posting and withdrawals throughout the life of the contract. In this set-up, MarginDEX will initiate the trades by matching traders with liquidity providers and then once the trade is initiated the rest of the settlement process will be managed by BlockMarghin

Acceptance Criteria

A web dashboard where a buy and a sell can be initiated by a trader and be automatically matched against the liquidity in the AMM

The trade is then passed onto the BlockMargin interface to manage the settlement of the trade until maturity. The BlockMargin interface is available at https://blockmargin.app/trade

Evidence of Completion

- Liquidity provided by 5 different wallets on the testnet

- Successfully executed a batch of 10 trades which are then passed onto BlockMargin

A video walkthrough of the evidence

Delivery Month

12

Cost

24996

Progress

100 %

[Final Pitch] Budget & Costs

Please provide a cost breakdown of the proposed work and resources

The budget is estimated based on 40 hours per week and 4 weeks per month.

Milestone 1: Design AMM models

- One Senior developer 40h per week for 4 weeks @ $60/h

- One Senior derivatives expert 40h per week for 4 weeks @ $60/h

Total 19,200 USD

Milestone 2: Implement Cluster of AMMs

- One Senior developer 40h per week for 6 weeks @ $60/h

- One Senior derivatives expert 40h per week for 2 weeks @ $60/h

Total 19,200 USD

Milestone 3: Implement Curve-wide AMM

- One Senior developer 40h per week for 6 weeks @ $60/h

- One Senior derivatives expert 40h per week for 2 weeks @ $60/h

Total 19,200 USD

Milestone 4: Integration with BlockMargin and Testnet Launch

- One Senior developer 40h per week for 8 weeks @ $60/h

Total 19,200 USD

Business development, server costs and Marketing:

Travel to London and Amsterdam to demo the product to financial institutions and brokers.

A booth/stand at Web-summit to showcase the product and network. The team has been previously invited to Web-summit to for other projects we built and we would repeat the same with MarginDEX

Travel costs to Amsterdam and London @ 750 USD per trip x2

Web-summit booth @ 1,500

Server costs @ 15 USD per month for 12 months

Total 3,180 USD

Total for project 79,980 USD

A conservative ADAUSD exchange rate of 0.8 is assumed for the budgeting. At this level we are happy to hold ADA if the price drops significantly below that

Total for project in ada 99,975

[Final Pitch] Value for Money

How does the cost of the project represent value for the Cardano ecosystem?

MarginDEX represents a high-value use of funds because it brings the world’s largest financial market - Interest Rate Derivatives - onto Cardano, creating a first-of-its-kind DeFi application. By funding this project, the Cardano ecosystem gains a transparent, permissionless, and automated trading platform for instruments historically restricted to large institutions. A Cardano-native financial infrastructure not available on any other blockchain.

This innovation demonstrates Cardano’s capability to handle complex financial products, increasing adoption by financial institutions, attracting liquidity, and expanding Total Value Locked (TVL). The project also fosters DeFi growth by enabling smaller corporates and retail participants - largely excluded from this market - to trade the products efficiently.

The proposal enables us to work on R&D and deployment of the AMM models (Cluster and Curve-wide), integration with BlockMargin, and operational testnet activity - all of which are critical for demonstrating viability and attracting future institutional adoption. Successful execution will generate network effects, showcasing Cardano as a platform for high-value, real-world financial applications.

The team has decades of combined experience in derivatives trading and blockchain development, has successfully delivered multiple prior Catalyst-funded projects, and is deeply familiar with AMM DEXs on Cardano and other Blockchains.

The prototype and MVP are already partially operational on testnet (BlockMargin and simple order book), which reduces risk and ensures that each milestone produces a demonstrable output.

The budget reflects typical industry contract rates:

- $60/hour for senior developers. In line with global blockchain developer contract rates, often ranging from $50–$100/h

- $60/hour for data experts. In line with specialist quantitative finance/data engineering roles, in Western markets.

- $30/hour for juniors. In line with typical $35–$50/h junior blockchain dev rates.

Typical range estimated from glassdoor.com

[Required Acknowledgements] Consent & Confirmation

Terms and Conditions:

Yes

Team

Project Lead: Dmitry Shibaev

https://www.linkedin.com/in/shibaev/

Dmitry Shibaev is an experienced Project Lead and Senior Developer with a proven track record in both big tech and financial markets. His expertise spans 5 years in delivering large-scale SAP projects for energy companies in southern Europe and 15 years in financial markets, where he successfully led significant projects at a prominent investment bank across London, Singapore, and Amsterdam.

Open source contributor: https://github.com/dynamicstrategies

Speaker at IntersectMBO and Cardano Foundations forums:

- https://www.youtube.com/watch?v=NiUZmqx-F1Y

- https://www.linkedin.com/feed/update/urn:li:activity:7300875856212590593/

University Lecturer: https://www.linkedin.com/feed/update/urn:li:activity:7360747744832950272/

Recognized by the Portuguese business journal for building innovative projects on blockchains: https://www.jornaldenegocios.pt/negocios-em-rede/detalhe/queremos-atrair-fixar-e-desenvolver-talento-em-cascais

Creator of the Cardano’s Staking Reward Calculator: https://cardano.org/calculator/

Key in delivering previously funded Catalyst projects

- CardanoBeam - https://projectcatalyst.io/funds/8/dapps-and-integrations/cardano-beam-gps-based-assets

- Education Material for Workshops - https://projectcatalyst.io/funds/8/grow-africa-grow-cardano/education-material-for-workshops

- Blueprint for Investment Funds - https://projectcatalyst.io/funds/9/legal-and-financial-implementations/blueprint-for-investment-funds

- Credit Card Gateway - https://projectcatalyst.io/funds/11/cardano-open-developers/credit-card-gateway

- BlockMargin - proof of concept on the testnet - https://projectcatalyst.io/funds/11/cardano-use-cases-concept/blockmargin-interest-rate-futures-on-cardano

Full stack Web2, Web3 and Mobile developer behind:

Regulatory Expert: Sergio Rodrigues

https://www.linkedin.com/in/sergio-vieira-rodrigues-819bb8/

Sergio has 20 years of experience in systems implementation in Large International Banks. He is also a Banking Regulatory Expert with experience dealing with financial regulators across Europe

Junior Developer: Vlad Mikirtumov

https://www.linkedin.com/in/vmikirtumov/

Aerospace Engineer by education. Experience project manager and test engineer at ASML microchips and HODL funds

Data Expert: Paulo Rosario

https://www.linkedin.com/in/paulorosario/

Paulo is an experienced Economist/Data Scientist/Econometrician with a demonstrated history of working with data (from econometrics to Machine learning) to produce business insights and actionable knowledge.

He previously held senior data role at M&G and Skytra - a data company of Airbus